KYC and AML compliance is critical for preventing fraud, money laundering, and regulatory penalties in financial services.

Key KYC and AML compliance challenges include evolving regulations, identity verification, data management, false positives, and cross-border complexity.

Organizations must adopt risk-based approaches, automation, and centralized systems to improve compliance efficiency and accuracy.

Continuous employee training is essential to ensure teams can identify risks and stay aligned with changing AML and KYC requirements.

A structured approach like the SHIELD framework helps organizations manage compliance proactively, improve audit readiness, and reduce operational risk.

KYC (Know Your Customer) and AML (Anti-Money Laundering) are no longer optional in financial services—they are essential for preventing fraud and financial crime. With global money laundering estimated at 2–5% of GDP, organizations face growing pressure to strengthen compliance while managing complex regulations and large volumes of customer data.

At the same time, institutions must balance strict verification with seamless customer experience. These ongoing KYC and AML compliance challenges make regulatory compliance a continuous and evolving process.

While KYC and AML play a critical role, they represent only a fraction of the broader financial services compliance landscape that organizations must manage today.

Understanding Financial Services Compliance

Financial services compliance refers to the systems, processes, and controls that ensure financial institutions follow regulatory, legal, and ethical standards across markets.

In simple terms, it ensures:

Organizations operate legally

Customer data is protected

Financial crimes are prevented

Risks are monitored and controlled

Compliance today is no longer a static checklist. It is a continuous, data-driven function that evolves with regulatory changes, digital transformation, and global operations.

Why Compliance is Increasingly Complex

Area | What’s Changing | Impact on Organizations |

|---|---|---|

Regulations | Frequent updates across regions | Constant monitoring required |

Technology | Rise of digital banking & cloud | Higher cyber and data risks |

Globalization | Multi-country operations | Multiple compliance frameworks |

Customer Data | Stricter privacy laws | Higher accountability |

Financial Crime | Sophisticated fraud tactics | Advanced detection needed |

What Are Financial Services Compliance Challenges?

Financial services compliance challenges are the operational, regulatory, and technological barriers organizations face while trying to meet evolving legal and risk requirements.

These challenges typically arise due to:

Rapid regulatory changes

Complex global operations

Increasing cybersecurity threats

Data privacy enforcement

Evolving financial crime risks

KYC and AML in Financial Services Compliance

KYC (Know Your Customer) and AML (Anti-Money Laundering) are core components of financial services compliance, focusing on identity verification, risk assessment, and transaction monitoring. While financial services compliance covers a wide range of regulatory requirements, KYC and AML remain among the most operationally complex and high-risk areas.

To manage these challenges effectively, organizations must invest in structured AML KYC training that equips teams to apply compliance practices in real-world scenarios. As a result, financial institutions can strengthen compliance frameworks and reduce exposure to financial crime.

Facing KYC and AML Compliance Challenges: Solutions That Work

To manage modern KYC & AML challenges, financial institutions must adopt smarter, data-driven, and technology-supported solutions.

1. AML and KYC Regulatory Compliance Challenges

Challenge:

Constant updates in AML and KYC regulations across jurisdictions

Difficulty aligning internal policies with evolving regulatory requirements

High risk of penalties due to delayed compliance updates

Lack of real-time visibility into regulatory changes

How to Solve:

Build a centralized regulatory repository mapping AML/KYC rules to business processes

Implement a regulatory change management workflow with defined ownership

Break regulations into clear SOPs and actionable policies

Deliver frequent, bite-sized training updates for employees

Use compliance dashboards to track implementation and gaps

Conduct periodic internal audits to ensure alignment with latest regulations

Key takeaway: Shift from reactive updates to structured compliance management

2. KYC Customer Identity Verification Challenges

Challenge:

Difficulty verifying customer identity in digital onboarding

Increased risk of fake or forged identity documents

Inconsistent verification processes across channels

Delays in onboarding due to manual KYC checks

How to Solve:

Adopt a risk-based KYC approach (low-risk vs high-risk customers)

Use digital verification tools (biometrics, document validation)

Standardize identity verification across all onboarding channels

Enable real-time validation checks for incomplete or suspicious data

Reduce manual intervention through automation in onboarding workflows

Continuously refine onboarding process based on drop-off insights

Key takeaway: Balance strong verification with seamless onboarding

Continuous learning support through platforms like Calibr can help teams improve accuracy in KYC verification and reduce onboarding errors.

3. KYC Data Management and Accuracy Challenges

Challenge:

Handling large volumes of customer data across systems

Incomplete or inconsistent KYC data records

Difficulty maintaining a single source of truth

Challenges in retrieving data for audits and reporting

How to Solve:

Create a centralized customer data system (single source of truth)

Implement data validation and cleansing processes regularly

Define clear ownership for data management across teams

Maintain structured data storage for easy audit access

Conduct regular data quality audits to identify inconsistencies

Ensure integration between systems to avoid duplication

Key takeaway: Accurate data is the foundation of effective compliance

4. AML Compliance Challenges in Transaction Monitoring

Challenge:

High volume of alerts generated by AML systems

Excessive false positives impacting efficiency

Difficulty identifying truly suspicious transactions

Delays in investigating and reporting suspicious activity

How to Solve:

Implement risk-based transaction monitoring models

Use advanced analytics and behavioral pattern detection

Continuously update monitoring rules based on new fraud patterns

Reduce false positives through rule optimization and tuning

Establish clear workflows for alert investigation and reporting

Create feedback loops to improve detection accuracy over time

Key takeaway: Smarter systems reduce noise and improve detection

For example, Scenario-based training delivered through platforms like Calibr can further strengthen employees’ ability to identify suspicious transactions in real-world situations.

5. Data Privacy Challenges in KYC and AML Compliance

Challenge:

Managing sensitive customer data across jurisdictions

Ensuring compliance with data protection laws (GDPR, etc.)

Weak consent and audit tracking mechanisms

Risk of data breaches and regulatory penalties

How to Solve:

Map data lifecycle (collection, storage, usage, deletion)

Implement role-based access controls (RBAC)

Maintain consent management systems and audit trails

Regularly update data retention and deletion policies

Conduct privacy impact assessments (PIA)

Train employees on secure data handling practices

Key takeaway: Strong governance ensures data protection and compliance

6. KYC Onboarding and Customer Experience Challenges

Challenge:

Lengthy and complex KYC onboarding processes

High customer drop-off rates during verification

Balancing strict compliance with seamless experience

Inefficient manual processes slowing onboarding

How to Solve:

Introduce digital onboarding workflows to automate processes

Apply risk-based onboarding to simplify low-risk customer journeys

Reduce redundant steps to improve onboarding speed

Monitor onboarding KPIs (completion rate, drop-offs)

Optimize processes using customer feedback and analytics

Ensure compliance checks are embedded without friction

Key takeaway: Faster onboarding without compromising compliance

7. AML Financial Crime Detection Challenges

Challenge:

Rapidly evolving money laundering techniques

Use of digital channels and emerging technologies by criminals

Difficulty updating detection systems in real time

Gaps between regulatory expectations and detection capability

How to Solve:

Implement dynamic risk assessment models

Continuously update detection strategies based on emerging threats

Train employees using real-world suspicious activity scenarios

Strengthen collaboration between compliance and risk teams

Use intelligence sources to stay updated on financial crime trends

Conduct periodic reviews of detection effectiveness

Key takeaway: Detection must evolve with financial crime

8. Cross-Border KYC and AML Compliance Challenges

Challenge:

Different AML and KYC regulations across countries

Difficulty standardizing compliance processes globally

Lack of clarity on jurisdiction-specific requirements

Increased risk of non-compliance in international operations

How to Solve:

Establish a central compliance framework with local adaptations

Develop jurisdiction-specific AML/KYC guidelines

Assign regional compliance ownership

Maintain clear documentation for regulatory audits

Track regulatory differences through structured mapping

Standardize processes while allowing flexibility

Key takeaway: Balance global consistency with local compliance

9. Third-Party KYC and AML Compliance Challenges

Challenge:

Dependence on external KYC verification providers

Limited visibility into vendor compliance practices

Inconsistent due diligence across third parties

Regulatory risk remains with the organization

How to Solve:

Build a vendor risk management framework

Conduct thorough due diligence before onboarding vendors

Categorize vendors based on risk level

Monitor vendor compliance performance regularly

Include audit rights and compliance clauses in contracts

Review vendor performance periodically

Key takeaway: Third-party risk requires continuous oversight

10. KYC and AML Training and Skill Gap Challenges

Lack of skilled professionals in AML and KYC compliance

Employees unable to identify suspicious activities effectively

Outdated or ineffective compliance training programs

Low engagement in compliance training initiatives

How to Solve:

Provide role-based compliance training programs

Use scenario-based learning for real-world application

Deliver continuous learning instead of one-time training

Track training effectiveness through assessments

Align training with evolving AML/KYC requirements

Encourage a culture of continuous learning and awareness

Key takeaway: Skilled teams are critical for effective compliance

Platforms like Calibr also help organizations deliver role-based compliance training and track learning effectiveness, improving overall workforce readiness.

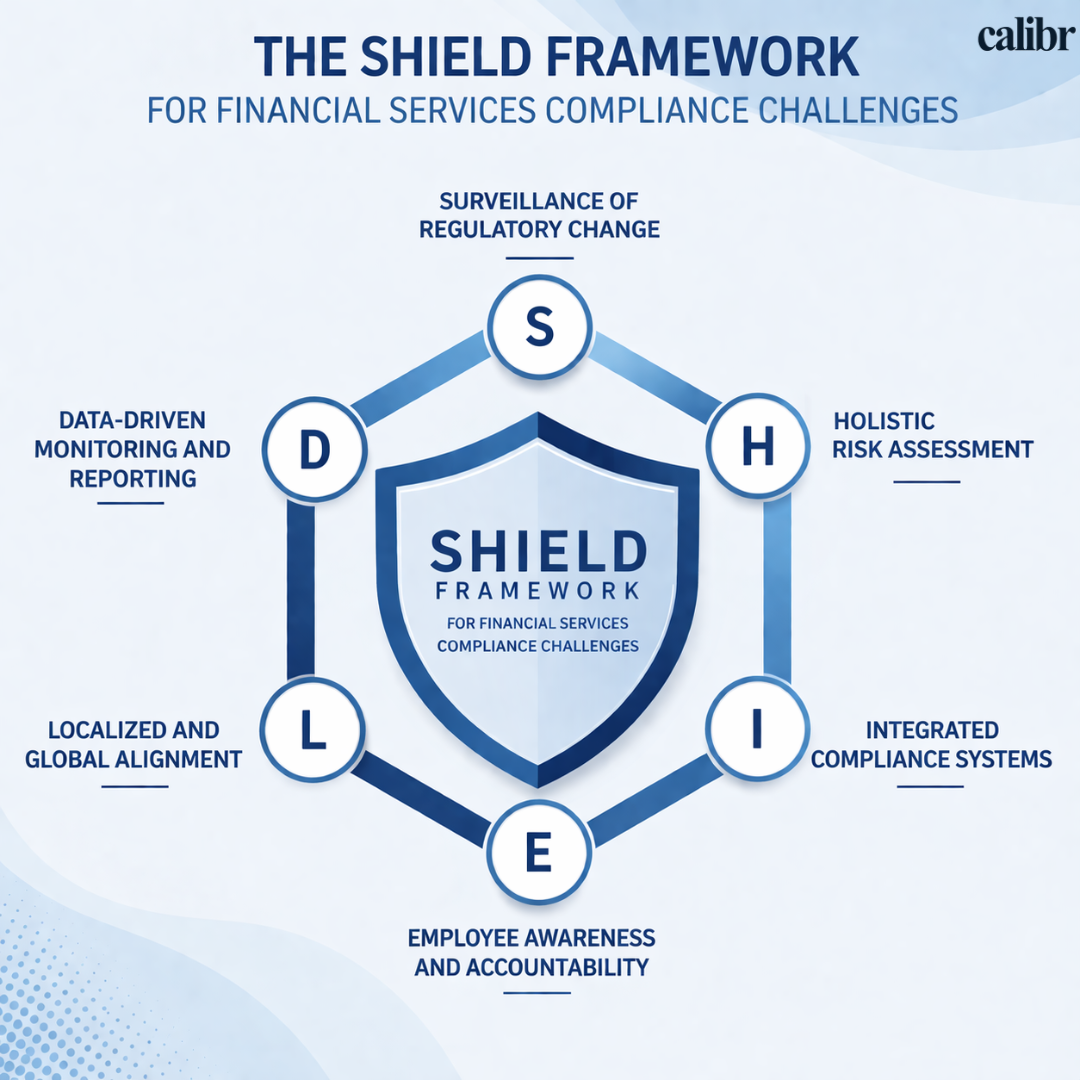

The SHIELD Framework for Financial Services Compliance Challenges

A Practical Model to Manage Financial Services Compliance Challenges Effectively

The SHIELD Framework helps organizations systematically address financial services compliance challenges by focusing on six critical pillars that drive resilience, accountability, and measurable outcomes.

S — Surveillance of Regulatory Change

Continuously monitor and interpret regulatory updates across jurisdictions.

Track global and local regulatory changes in real time

Map regulations to internal policies and processes

Assign clear ownership for regulatory updates

Ensures organizations stay ahead of evolving financial services compliance challenges instead of reacting late

H — Holistic Risk Assessment

Identify and evaluate risks across operations, technology, and third parties.

Conduct enterprise-wide compliance risk assessments

Prioritize risks based on impact and likelihood

Align compliance with overall business risk strategy

Helps focus resources on the most critical compliance challenges

I — Integrated Compliance Systems

Unify compliance processes, data, and reporting into a centralized system.

Maintain a single source of truth for policies and controls

Integrate compliance with business workflows

Enable cross-functional collaboration

Reduces fragmentation, a major cause of financial services compliance challenges

E — Employee Awareness and Accountability

Ensure employees understand their compliance responsibilities.

Deliver role-based compliance training

Define clear accountability structures

Reinforce compliance through continuous communication

Turns compliance from a policy into daily behavior

L — Localized and Global Alignment

Balance global standards with local regulatory requirements.

Adapt compliance policies for regional laws

Maintain consistency across international operations

Monitor jurisdiction-specific obligations

Critical for managing cross-border financial services compliance challenges

D — Data-Driven Monitoring and Reporting

Measure compliance effectiveness using real-time insights.

Track KPIs such as incidents, response times, and audit outcomes

Use analytics to identify gaps and risks

Generate board-level compliance reports

Enables organizations to prove effectiveness and improve continuously

Frequently Asked Questions (FAQs)

What are the biggest KYC and AML compliance challenges?

The biggest KYC and AML compliance challenges include evolving regulatory requirements, identity verification complexity, high volumes of customer data, false positives in transaction monitoring, cross-border compliance issues, and lack of skilled workforce.

Why is KYC and AML compliance important in financial services?

KYC and AML compliance is important because it helps financial institutions prevent fraud, detect money laundering activities, protect customer data, and avoid regulatory penalties while maintaining trust with regulators and customers.

How can financial institutions improve KYC and AML compliance?

Organizations can improve KYC and AML compliance by adopting risk-based verification, automating onboarding and monitoring processes, centralizing data systems, and providing continuous compliance training to employees.

What is the difference between KYC and AML?

KYC focuses on verifying customer identity and assessing risk during onboarding, while AML involves monitoring transactions and detecting suspicious activities to prevent financial crimes.

How does technology help in KYC and AML compliance?

Technology improves KYC and AML compliance by enabling automated identity verification, advanced transaction monitoring, real-time data analysis, and reducing manual errors and false positives.

How can organizations measure KYC and AML compliance effectiveness?

Organizations can measure compliance effectiveness using KPIs such as onboarding completion rates, reduction in false positives, faster alert resolution, audit performance, and employee understanding of compliance requirements.

Bringing it all together

Effectively managing KYC and AML compliance challenges is essential for building resilient and future-ready financial institutions. As regulatory requirements evolve and financial crime becomes more sophisticated, organizations must adopt a proactive and structured approach to compliance.

This includes staying aligned with changing regulations, strengthening data and onboarding processes, and equipping teams with the right knowledge to identify and manage risks. A well-designed KYC and AML framework ensures transparency, auditability, and consistent compliance across the organization.

Ultimately, organizations that treat compliance as a continuous, data-driven function—not just a regulatory requirement—are better positioned to reduce risk, improve operational efficiency, and maintain trust with regulators and customers.

Organizations can also leverage adaptive learning platforms like Calibr to keep teams updated on evolving KYC and AML requirements and improve overall compliance readiness.

Next Steps:

Take your compliance training to the next level by,

Explore how your organization can achieve smarter, more effective KYC and AML compliance.

Vivetha is a digital marketing professional specializing in content marketing and SEO. She focuses on developing optimized, high-quality content that improves search visibility, supports brand objectives, and drives measurable results. With a structured and analytical approach, she ensures content aligns with business and audience needs.